Normal backwardation

Normal backwardation, also sometimes called backwardation, is the market condition wherein the price of a forward or futures contract is trading below the expected spot price at contract maturity.[1] The resulting futures or forward curve would typically be downward sloping (i.e. "inverted"), since contracts for further dates would typically trade at even lower prices.[2] In practice, the expected future spot price is unknown, and the term "backwardation" may be used to refer to "positive basis", which occurs when the current spot price exceeds the price of the future.[3]:22

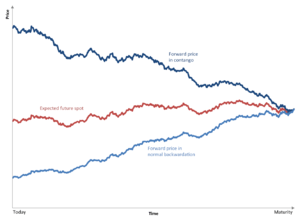

The opposite market condition to normal backwardation is known as contango. Similarly, in practice the term may be used to refer to "negative basis" where the current spot price is below the future price.[3]

A backwardation starts when the difference between the forward price and the spot price is less than the cost of carry, or when there can be no delivery arbitrage because the asset is not currently available for purchase.

Futures contract price includes compensation for the risk transferred from the asset holder. This makes actual price on expiry to be lower than futures contract price. Backwardation very seldom arises in money commodities like gold or silver. In the early 1980s, there was a one-day backwardation in silver while some metal was physically moved from COMEX to CBOT warehouses. Gold has historically been positive with exception for momentary backwardations (hours) since gold futures started trading on the Winnipeg Commodity Exchange in 1972.[4]

The term is sometimes applied to forward prices other than those of futures contracts, when analogous price patterns arise. For example, if it costs more to lease silver for 30 days than for 60 days, it might be said that the silver lease rates are "in backwardation". Negative lease rates for silver may indicate bullion banks require a risk premium for selling silver futures into the market.

Occurrence

This is the case of a convenience yield that is greater than the risk free rate and the carrying costs.

It is argued that backwardation is abnormal, and suggests supply insufficiencies in the corresponding (physical) spot market. However, many commodities markets are frequently in backwardation, especially when the seasonal aspect is taken into consideration, e.g., perishable and/or soft commodities.

In Treatise on Money (1930, chapter 29), economist John Maynard Keynes argued that in commodity markets, backwardation is not an abnormal market situation, but rather arises naturally as "normal backwardation" from the fact that producers of commodities are more prone to hedge their price risk than consumers. The academic dispute on the subject continues to this day.[5]

Examples

Notable examples of backwardation include:

- Copper circa 1990, apparently arising from market manipulation by Yasuo Hamanaka of Sumitomo Corporation in what has come to be called the "Sumitomo copper affair".

- A more recent example of market backwardation – In 2013, the wholesale commercial gas market entered backwardation during the month of March. The 2-year contract prices fell below the price of 1-year contracts.[6]

Origin of term: London Stock Exchange

Like contango, the term originated in mid-19th century England, originating from "backward".

In that era on the London Stock Exchange, backwardation was a fee paid by a seller wishing to defer delivering stock they had sold. This fee was paid either to the buyer, or to a third party who lent stock to the seller.

The purpose was normally speculative, allowing short selling. Settlement days were on a fixed schedule (such as fortnightly) and a short seller did not have to deliver stock until the following settlement day, and on that day could "carry over" their position to the next by paying a backwardation fee. This practice was common before 1930, but came to be used less and less, particularly since options were reintroduced in 1958.

The fee here did not indicate a near-term shortage of stock the way backwardation means today, it was more like a "lease rate", the cost of borrowing a stock or commodity for a period of time.

In more recent years, a backwardation in equities quoted on the London Stock Exchange has come to signify the unusual occurrence of an individual equities quote whereby the bid appears to be higher than the offer. This (of course) cannot occur for electronically traded stocks via SETS or SETS MM but only for quote-driven stocks (SEAQ)

Normal backwardation vs. backwardation

The term backwardation, when used without the qualifier "normal", can be somewhat ambiguous. Although sometimes used as a synonym for normal backwardation (where a futures contract price is lower than the expected spot price at contract maturity), it may also refer to the situation where a futures contract price is merely lower than the current spot price.

See also

References

| Wikisource has the text of the 1911 Encyclopædia Britannica article Backwardation. |

- ↑ Contango Vs. Normal Backwardation, Investopedia

- ↑ The curves in question plot market prices for various contracts at different maturities—cf. yield curve

- 1 2 Gorton G, Rouwenhorst KG. Facts and Fantasies about Commodity Futures. NBER.

- ↑ Antal E. Fekete (2 December 2008). "RED ALERT: GOLD BACKWARDATION!!!(page 3)" (PDF). Retrieved 20 December 2008.

- ↑ Zvi Bodie & Victor Rosansky, "Risk and Return in Commodity Futures", FINANCIAL ANALYSTS' JOURNAL (May/June 1980)

- ↑ http://www.apolloenergy.co.uk/wholesale-gas-market-an-important-update/

- Encyclopædia Britannica, eleventh edition (1911), articles Backwardation, Contango and Stock Exchange, and fifteenth edition (1974), articles Contango and Backwardation and Stock Market.

- Modern Market Manipulation, Mike Riess, 2003, paper at the International Precious Metals Institute 27th Annual Conference

- LME launches and investigation in primary aluminium trading, London Metal Exchange advice to members 15 January 1999, reproduced at aluNET International

- New Orleans – Temporary Suspension of Warrants, London Metal Exchange press release 6 September 2005.

- investopedia Website, Articles on Contango and Backwardation and Stock Market.